Before I share a single number, let me be transparent: I advise clients in both markets. This is not a case for one over the other. It is a framework to help you ask the right question — what do you expect this property to bring you? — before choosing where to invest.

All figures below are sourced directly from official Malaysian government data. No third-party estimates. No developer marketing materials.

NAPIC Property Market Status Report H1 2025 — Valuation and Property Services Department, Ministry of Finance Malaysia

The numbers side by side

| Indicator | Kuala Lumpur City (TRX corridor) | Johor Bahru City (RTS corridor) |

|---|---|---|

| Entry PSF | RM1,000–1,400 | RM850–1,200 (new launches near RTS hitting RM1,200) |

| Size at RM800k | ~600–700 sq ft | ~700–900 sq ft (at RM900–1,100 psf) |

| Gross rental yield | 4–5% | 5.24% city average (range: 3.23%–9.07%) |

| Economic base | Diversified — finance, tech, MNCs, government, education | Primarily Singapore-proximity driven |

| Key demand catalyst | TRX, Bandar Malaysia, Monash University, PwC HQ | RTS Link (target: Jan 2027), JS-SEZ |

| Residential overhang | 3,643 units (WP KL) — national high | 3,209 units |

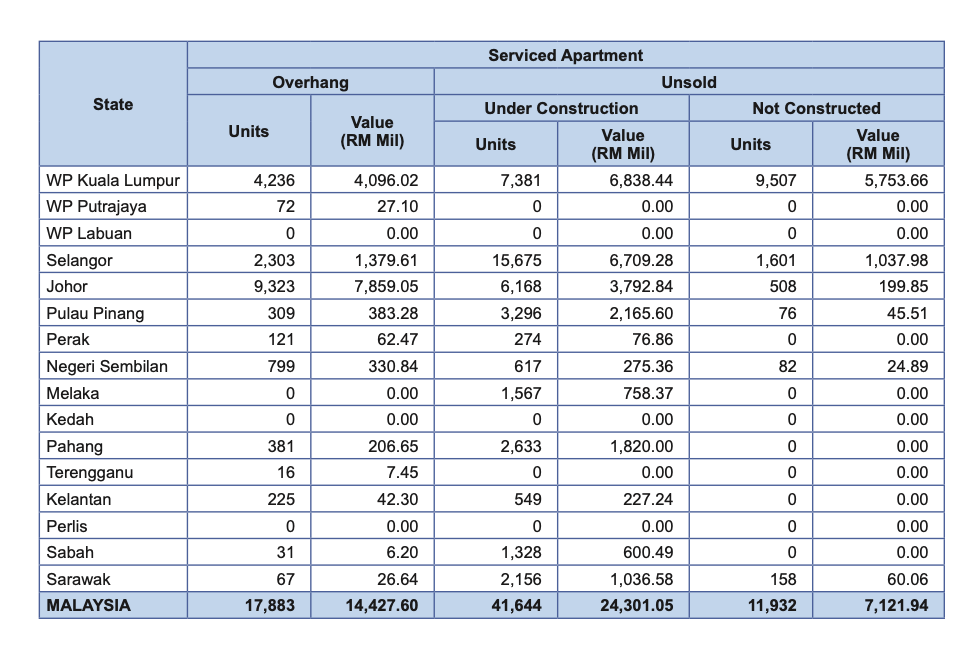

| Serviced apartment overhang | 4,236 units | 9,323 units — 52% of entire national total |

A note on the JB PSF figure: it tells a two-part story. Existing city centre transactions in Johor Bahru are running RM850–925 psf, while new launches near the RTS corridor are already hitting RM1,200 psf. That gap is entirely driven by speculation on the RTS premium — not by current rental demand or occupancy. Investors comparing entry PSF between KL and JB should ask which of these two JB numbers they are actually being quoted.

Source: NAPIC Property Market Status Report H1 2025, Valuation and Property Services Department, Ministry of Finance Malaysia. Page 8, Serviced Apartment Summary Table. View official PDF →

What this data actually means

Johor's residential overhang (3,209 units) is lower than KL's (3,643). On the surface, that looks fine. But the critical number is the serviced apartment overhang — the exact product category being heavily marketed to investors near the RTS corridor. Johor holds 9,323 of the 17,883 nationally unsold serviced apartments. That is more than half the entire country's unsold serviced apartment stock sitting in one state.

These are completed units — built, certificated, and sitting empty for more than 9 months. The wave that was supposed to absorb them — cross-border commuters, Singaporean buyers — has not arrived at the volume developers anticipated.

The appreciation near the RTS corridor was priced in before the RTS opened. That is the risk — not that the infrastructure fails, but that the market already front-loaded all the upside.

The RTS Link — current status

The RTS Link is on track. As of April 2026, Malaysia's Transport Minister confirmed 90% project completion, with operations targeting January 2027. The project has reached this stage without significant construction delays — a notable achievement for a cross-border infrastructure project of this scale.

What investors should understand: properties near Bukit Chagar and the RTS corridor have already risen 40–50% since 2020. The RTS hasn't opened yet — but the price has. When January 2027 arrives and the train starts running, the question will not be "will this area grow?" It will be "what is left to grow after five years of speculation?"

Source: The Independent SG, April 7 2026 — JB-SG RTS Link enters final phase →

Where each market makes sense

- Multiple demand drivers — not dependent on a single catalyst

- 166 years of economic compounding

- TRX at district-maturity discount vs KLCC peers

- Monash (2032) and PwC HQ (2029) yet to materialise

- Deeper resale market and more liquid exits

- Landed property in established areas — safer bet than high-rise

- Long hold period (10+ years) absorbs short-term correction risk

- JS-SEZ creating genuine economic diversification

- Avoid: serviced apartments above RM700k near RTS marketed as "ready to rent"

- Foreign buyer stamp duty now 8% — reduces Singaporean demand pressure

The honest conclusion

This is not Kuala Lumpur good, Johor Bahru bad. Both markets have genuine opportunities and genuine risks. The difference is in the nature of those risks.

Kuala Lumpur's risk is valuation — you are paying for an established market with less upside compression. Johor Bahru's risk is concentration — one state holding half the country's unsold serviced apartments, with a buyer pool that is 40% foreign and sensitive to a single infrastructure timeline.

The right market depends entirely on what you expect the property to bring you, and how long you are prepared to wait for it. Those two questions — purpose and timeline — should come before any comparison of PSF or yield.

If you are unsure which answer applies to you, that is exactly the conversation worth having before you sign anything.

1. NAPIC H1 2025 Property Market Status Report — Valuation and Property Services Department, Ministry of Finance Malaysia

2. NAPIC Q1 2025 Snapshot — napic.jpph.gov.my

3. Malaysia Transport Minister statement on RTS completion — CNA/NST via The Independent SG, April 2026

4. RTS Link official project details — Land Transport Authority Singapore & MRT Corp Malaysia

Not sure which market fits your goals?

The right answer depends on what you expect the property to bring you — and how long you're prepared to wait. Book a 60-minute portfolio consultation and let's work through it properly.

Get in touch →